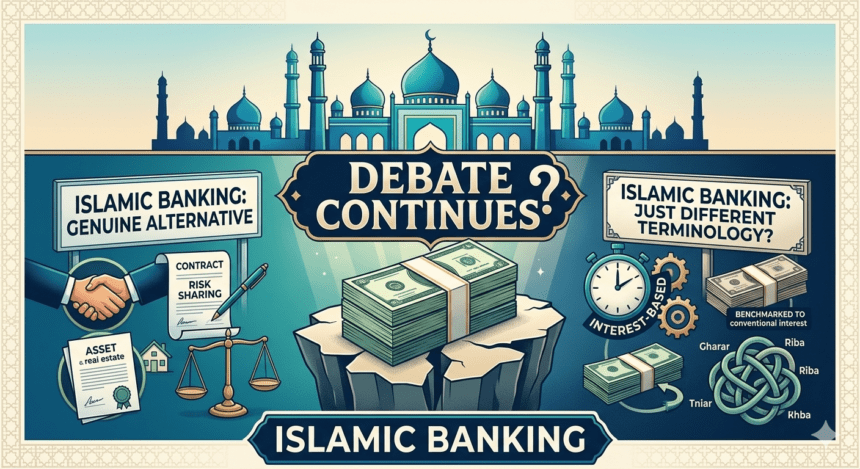

Islamabad: The question of whether Islamic banking is fundamentally different from conventional banking or merely a change in terminology continues to spark debate among economists, financial experts, and religious scholars.

Supporters of Islamic banking argue that the system is based on Shariah principles that prohibit interest (riba) and instead promote profit-sharing, asset-backed financing, and risk-sharing arrangements. They maintain that Islamic financial institutions operate under a distinct framework designed to ensure ethical and transparent transactions.

However, critics contend that many Islamic banking products ultimately produce financial outcomes similar to those of conventional banks. They argue that while contract structures and terminology may differ, customers often end up paying amounts comparable to interest-based financing.

Financial experts note that the key distinction lies in how transactions are structured. Islamic banking typically uses models such as profit-sharing partnerships, leasing agreements, and cost-plus financing arrangements rather than traditional interest-bearing loans. Nevertheless, some analysts believe the practical differences can be difficult for consumers to identify.

The debate has gained renewed attention as Islamic banking continues to expand globally, attracting customers seeking faith-based financial services while also drawing scrutiny from those questioning whether current practices fully reflect the principles on which the industry was founded.

Experts agree that the discussion is likely to continue as the sector evolves and regulators, scholars, and financial institutions seek to balance religious compliance with modern banking requirements.