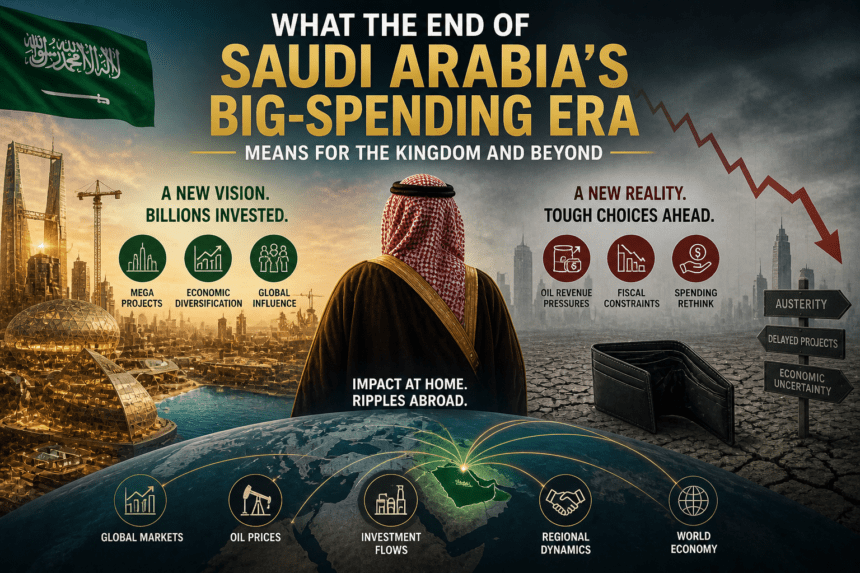

Saudi Arabia is not abandoning its transformation drive, but it is clearly entering a more selective phase. The kingdom’s 2026 budget projects a deficit of about 165 billion riyals (roughly $44 billion), even as officials say spending will be refocused on priority sectors rather than spread as widely as before. That shift matters because it suggests the era of almost unlimited, oil-backed spending is giving way to a more disciplined model shaped by lower oil revenue, borrowing needs and pressure to show results.

For Saudi Arabia itself, the biggest consequence is not a halt to Vision 2030, but a change in tempo. The government is still pushing diversification, tourism, logistics and industry, yet the emphasis is increasingly on implementation and prioritization. In plain terms, Riyadh now appears less willing to fund every grand ambition at full speed and more willing to decide which projects can realistically deliver economic value.

That is why the discussion around megaprojects has become so important. Recent reporting says Neom is being scaled back and redesigned, with its original vision trimmed in favor of a more practical industrial and infrastructure-led model. Reports also say some high-profile components have been delayed or reduced as officials reassess costs, timelines and returns. This does not mean the projects are dead. It means spectacle is giving way to triage.

The strain is showing up in the kingdom’s investment strategy more broadly. Recent coverage says Saudi decision-makers are rethinking some expensive overseas sports and branding bets while shifting more focus toward domestic priorities. That is a notable change because the kingdom’s spending surge was never only about construction at home; it was also about projecting influence abroad. A narrower spending approach could mean fewer splashy global deals and a sharper concentration on projects tied directly to tourism, jobs and long-term economic diversification inside Saudi Arabia.

For the kingdom, that could actually be stabilizing if it leads to better project discipline. Saudi Arabia still has substantial financial capacity and strong state backing, and the IMF has said the economy remains resilient with non-oil activity expanding, even as fiscal and external deficits persist over the medium term. So the story is not one of collapse. It is one of recalibration.

Beyond Saudi Arabia, the ripple effects could be real. Global contractors, consultants, sports ventures, tourism operators and suppliers that had built expectations around ever-rising Saudi demand may now face slower deal flow, delayed timelines or more aggressive cost scrutiny. Regional labor markets could also feel the shift if construction pipelines are stretched out rather than accelerated.

There is also a broader signal here for energy-rich states. Saudi Arabia’s experience shows the limits of financing vast economic transformation through oil wealth alone, especially when crude revenues soften and geopolitical uncertainty rises. The kingdom is still spending big by almost any standard, but the message now is different: ambition remains, yet money is being asked to work harder.